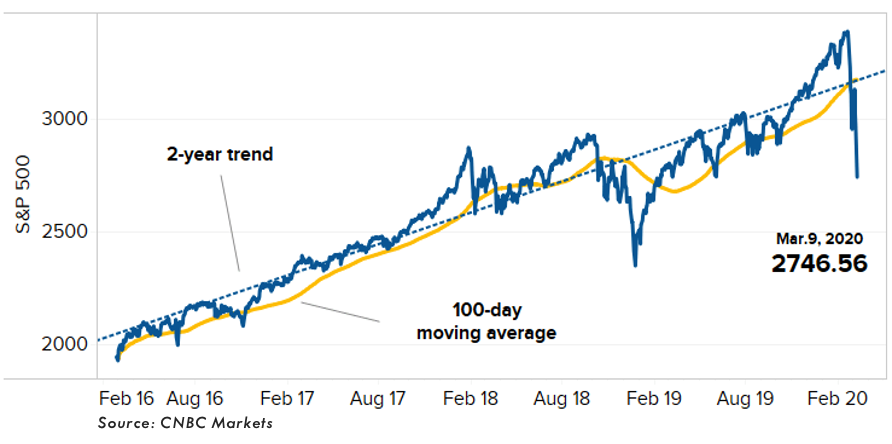

Record Highs and Record Lows

The year started as 2019 ended with equity valuations continuing to climb. Buoyed by the easing of trade war tensions between the world’s two leading economies, the S&P 500 reached an all-time high in mid-February. However, the celebrations were short-lived. Wall Street’s ever-changing level of concern over the coronavirus swung dramatically negative. The spread of the virus beyond China created fresh uncertainty for the global growth outlook and sparked volatility in financial markets. Economies came to a standstill in a bid to contain the virus, and markets tumbled 34% in just 22 days to record the fastest market correction in history.

Market Correction

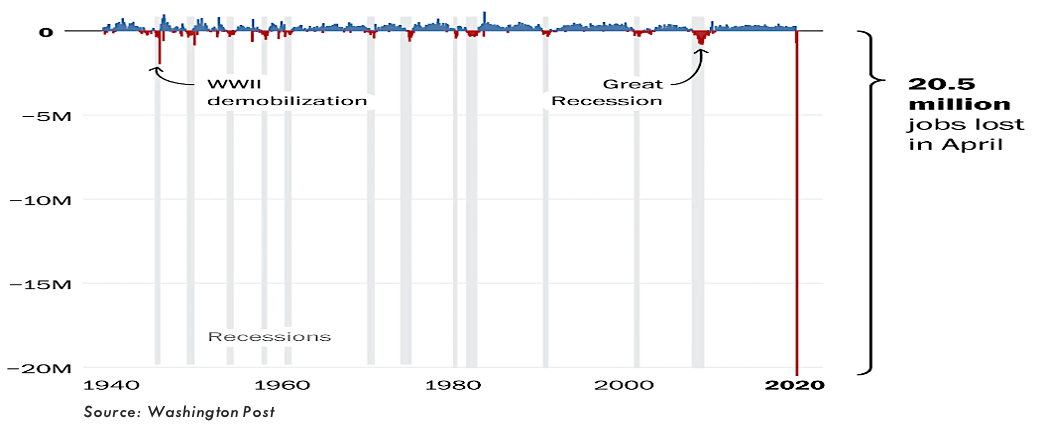

Economic data continued to deteriorate as the spread of the virus accelerated around the world. Central to this economic demise was the U.S. unemployment claims figures, which jumped by a staggering 20.5 million in April 2020 alone. To help put this into context, the largest monthly increase in unemployment figures during the Global Financial Crisis was 800,000. The worst month in history prior to this was a loss of 2 million jobs in September 1945 during WWII demobilization.

Monthly Job Gains or Losses In The U.S Since 1939

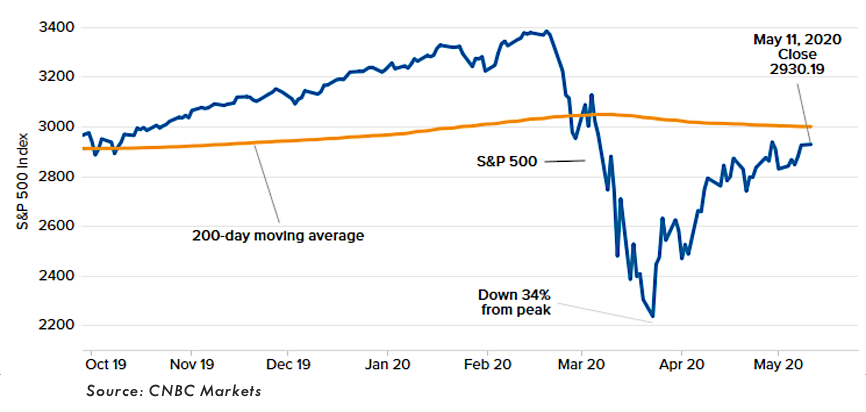

Despite the bleak economic fundamentals, share prices have staged a remarkable recovery. April was the S&P 500’s best month since January 1987, albeit after a March rout of about the same magnitude in the opposite direction. Having bottomed at 2,237 on March 23rd, the S&P 500 rallied by 32% by May 22nd. Technically, that has put shares back into a bull market, even though they have yet to regain all their pre-pandemic losses.

Coronavirus Comeback

But how have markets managed such as startling recovering in the middle of an economic collapse of historic proportions?

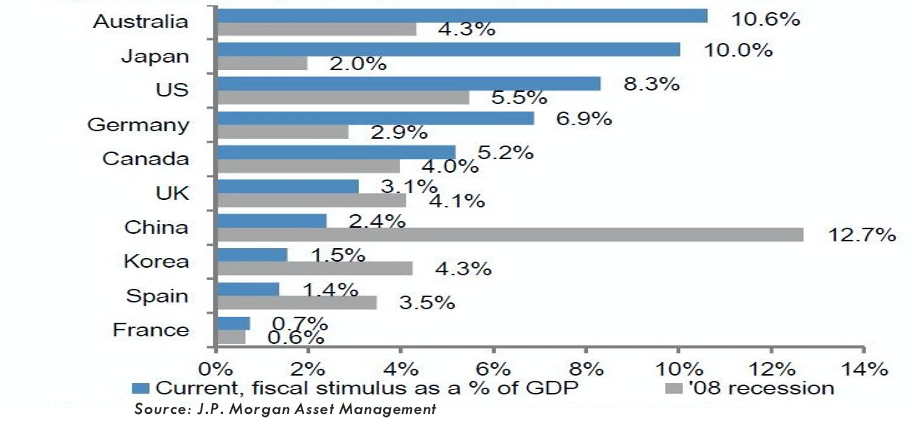

Unprecedented fiscal and monetary support has been at the heart of this market resurgence.

Policymakers around the globe have taken extraordinary steps to support financial markets with more than 50% of the world economy at or near the zero bound for interest rates as Central banks keep rates anchored and continue widespread quantitative easing policies to avoid the dreaded deflationary cycle and ensure market liquidity.

Fiscal stimulus by governments, which looks to soften the economic blow through targeted spending and relief, has far exceeded the Global financial crisis with 8 trillion dollars already dedicated to fighting the pandemic globally.

Fiscal Stimulus, as a % of GDP

CURRENT VS GFC

Right now, fiscal stimulus is replacing the income that is being lost by people who have been made redundant, supporting businesses who have seen their consumer base disappear in a bid to prop up aggregate demand. So far, this support has been successful in reducing the severity of the economic disruption as a result of the pandemic and has spurred investor confidence.

A Closer Look

Source: Bloomberg

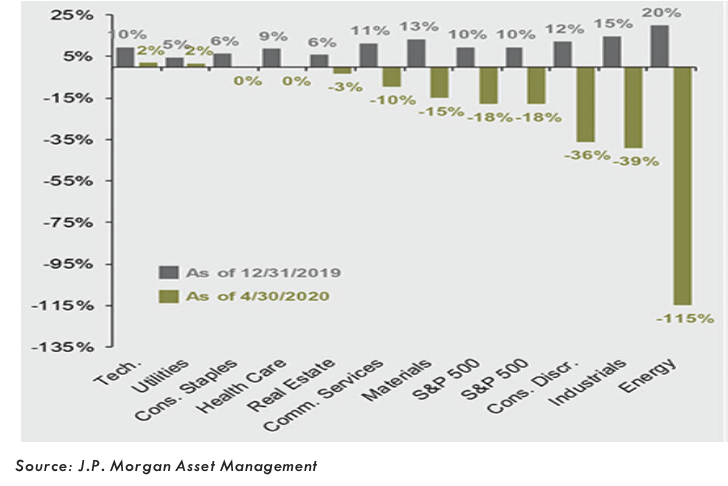

The S&P 500 has returned -8.0% YTD, recovering strongly following the initial coronavirus induced sell-off. Much of the rebound has been concentrated in the shares of five behemoth stocks. Facebook (+4%), Apple (+7%), Microsoft (+18%), Amazon (+30%) and Google (+5%). This group of companies accounts for approximately 20% of the S&P 500. The healthcare sector has also performed well, down less than 2% Since 1 January and representing 15% of the overall market cap of the S&P. A relatively small 3% exposure to Energy has also ensured that the S&P has not been overly exposed to the major drawdowns witnessed in the Energy Sector this year.

Source: Bloomberg

The tech-heavy Nasdaq Index is in positive territory YTD, up 4.4%, highlighting the Tech industry’s continued strength despite the current market uncertainty. While the tech industry’s outlook is encouraging, the return to positive territory is disproportionally dominated by ‘big tech’.

The NASDAQ is essentially the poster child for narrow market breadth, with the ten largest stocks gained $900 billion while the other 2,600 or so stocks in the Index collectively lost about $300 billion in Commodities, Gold lived up to its safe-haven credentials as a reliable store of value, up over 14% YTD, while oil suffered an entirely different faith.

As the global economy came to a virtual standstill, the demand for oil vanished, this, coupled with a poorly timed price war between OPEC and Russia saw oil prices collapse and oil futures run negative for the first time in history as storage capacity issues disrupted the supply/demand function within the oil industry. WTI Crude continued to rally last week, gaining over 11% but remains down nearly 65% YTD.

Market Outlook

It is important to remember that the Coronavirus is just the trigger that took the financial market into a period of correction. Record high valuations, anemic earnings figures, and underlying imbalances in financial markets have pointed towards the need for correction long before the coronavirus outbreak. While painful correction is required to generate a better and more sustainable outlook, long-term return expectations are improving. However, we are still cautious and expect further challenges over the coming quarters.

So, while the market performance of late would seem to suggest that the most severe economic slump in modern history doesn’t matter, that is not the case. Investors are merely focusing on the extensive fiscal and monetary support and its ability to prop up aggregate demand until everything returns to ‘normal’. Unfortunately, the success of this narrative is based heavily on the assumption of a shorter virus timeline allowing for a V-shaped recovery. With the economic data continuing to pile up and with the potential for a second wave of the virus still ever-present, a V-shaped recovery is far from certain, and as such, the coast is not yet clear in the short run.

The continuous earnings decline is a testament to this. Analysts’ earnings predictions for the S&P 500 in Q2 are now down 28% and negative for all quarters in 2020.

S&P 500 2020 Earnings Growth Estimates

At their most basic level, Stock prices are essentially a reflection of a companies’ future earnings. The above chart clearly illustrates the deterioration of earnings over the last year, but true to form, the stock market has continued its forward-looking trend and instead focuses on potential earnings growth into 2021 in a bid to justify current valuations. However, the longer these earnings remained suppressed by CoVID-19 uncertainty, the harder it becomes to sustain the most recent rally in the equity market.

What Does All This Mean for Investors?

While it is always important to look at the broader economic landscape, it is essential to assess how all these changes will affect specific asset classes and financial instruments in the future.

Equities

In the Equity Market, pitfalls still exist, but we have already witnessed the emergence of the ‘stay-at-home’ winners with technology, communication Services, and Health Care best positioned to take advantage of the current environment. For me, there are two main plays in today’s equity market for stock pickers. Future-proofed companies that have the capacity to grow regardless of the pandemic timeline is one. The second potential play is a riskier, value move, looking to take advantage of the lower price point of specific stocks in the hardest-hit industries, namely, Airlines, Cruise liners, event organizers, and hospitality. Don’t get drawn into the value-trap here, most of the stocks within these industries are cheap for a reason. The only relevant question you need to be asking yourself for now is, will this company survive? With this in mind, there may be some longer-term value in the more prominent players.

Fixed Income

For fixed-income investors, monetary stimulus has created a challenging landscape, with safe-haven bonds offering interest rates of close to zero, all but eliminating their upside protentional. As the economy moves past the CoVID-19 recession and begins to expand again, these interest rates will remain unattractive over the longer-term.

In High Yield markets, the market volatility of late has caused spreads to widen to their highest point since the Global Financial Crisis. While there may be individual opportunities in this space where careful selection can yield better returns, the potential for widespread defaults amongst high yield bonds is likely in the months ahead, so proceed with caution.

All-in-all, the fundamental changes to the fixed-income asset class as a result of monetary stimulus have continued to drive up bond valuation, effectively deteriorating the future returns previously on offer. The diversification benefits have not gone away, but longer-term investors may want to be underweight fixed-income as the economy re-emerges, opting instead for Alternative Investments such as precious metals, private equity, real estate, and venture capital.

Alternatives

As my faith in the longer-term sustainability of current monetary policies deteriorates, I have become increasingly interested in the likes of Gold and Bitcoin as a currency hedging play. With too much debt and not enough real growth, the current systems’ infinite ability to prop up aggregate demand in a bid to elongate our’ inflationary cycle’ is questionable at best. While the incentive structure will ensure that this structurally flawed approach continues to play out over the short-term, a longer-term currency hedging approach is still very appealing.

Gold vs. Bitcoin

Gold has lived up to the billing as the ultimate store of value historically speaking. With a 7.5 Trillion dollar market cap, it is a far more established asset class relative to bitcoin which currently has a market cap of $120 billion (bear in mind this figure may have changed dramatically in the time it takes to write this piece) which makes Gold the more sensible play for the risk-averse investor. For me, however, the sheer illiquidity of physical Gold is a significant deterrent, with larger orders potentially taking months to fill. While Bitcoin is not without its flaws, I feel it will be one of the major beneficiaries once governments realise they can’t endlessly prop-up economies through currency debasement.

The above article was written on behalf of Holdun, and has been written with personal views and as such may differ slightly from other published Holdun material.

Recent Comments